45. Weekly Market Recap: Key Movements & Insights

🕊️Doves vs. Hawks 🦅: Fed's Internal Split and Trump's Taunts Create a Choppy Week

Fed Uncertainty, Mideast Tensions Push S&P 500 to Weekly Loss

Wall Street ended a choppy week in negative territory as investors grappled with a mix of persistent geopolitical tensions, domestic policy uncertainty, and a divided Federal Reserve. The S&P 500 couldn't hold onto early gains, ultimately closing the week down as traders weighed hawkish signals from the Federal Open Market Committee (FOMC) against hints of a potential summer interest rate cut from a key Fed governor.

For the week, the S&P 500 fell 0.7%. The market's inability to gain traction, despite some late-week optimism, highlights a cautious investor sentiment. All eyes remain on the escalating conflict in the Middle East and the Federal Reserve's next moves as it navigates a complex economic landscape shaped by trade policy and concerns about inflation.

A Volatile Week on Wall Street

The week began on an optimistic note, with stocks rising on Monday on hopes for a potential de-escalation of the conflict in the Middle East. That sentiment proved short-lived, however, as the situation continued to develop, pushing the S&P 500 down 0.84% by Tuesday's close.

Wednesday brought an eagerly awaited announcement from the FOMC, which confirmed that the Fed would hold interest rates steady. The committee cited ongoing uncertainty surrounding tariffs and trade policy as a key factor in its decision. On the same day, U.S. Treasury yields saw a brief dip after May housing starts data came in below expectations.

Markets were closed on Thursday in observance of the Juneteenth holiday.

Some optimism returned to the market on Friday. The mood was lifted by news that the White House is still deliberating its involvement in the Middle East conflict, as well as new comments from Federal Reserve Governor Christopher Waller, who suggested the Fed could potentially cut interest rates as soon as July. Despite the late rally, the positive sentiment wasn't enough to pull the major indices into the green for the week.

Oil Pushes Higher, Gold Retreats

The ongoing conflict between Israel and Iran continued to ripple through commodity markets. Oil prices pushed higher for the third consecutive week, fueled by fears of a wider disruption to energy supplies. U.S. West Texas Intermediate (WTI) crude oil closed up 1.6% for the week. Analysts noted that while a worst-case scenario involving a shutdown of the Strait of Hormuz remains unlikely, the risk premium in oil prices is expected to persist until there are clear signs of de-escalation.

In contrast to oil, gold pulled back after a strong prior week. Despite the increased geopolitical uncertainty that typically favors safe-haven assets, gold fell 2.0% for the week.

Cryptocurrencies had a relatively quiet week. Bitcoin briefly dipped before trading back into its previous range, finishing the week down 1.9%. The market showed little reaction to the Senate's approval of the GENIUS Act, a bill aimed at establishing clear regulations for stablecoins.

Overall, energy minerals, consumer services, and finance were the strongest-performing sectors. Health technology, consumer non-durables, and process industries lag.

Fed in Focus as Rate Cut Debate Heats Up

The Federal Reserve remains a central focus for investors. While the official FOMC statement signaled a patient, wait-and-see approach, comments from Governor Waller on Friday introduced a more dovish narrative. Waller argued that signs of a softening labor market could justify a rate cut as soon as July to preempt a more significant downturn.

This apparent division comes as President Trump continues his public campaign for lower rates, recently calling Fed Chair Jerome Powell a "numbskull" while acknowledging his criticism makes it harder for the central bank to act. The Fed has maintained that its decisions are data-dependent and focused on its dual mandate of maximizing employment and stabilizing prices, independent of political pressure.

Upcoming Key Events:

Monday, June 23:

Earnings: Prosus N.V. (PRX), Naspers Limited (NPN)

Economic Data: Existing Home Sales

Tuesday, June 24:

Earnings: FedEx Corporation (FDX), Carnival Corporation & plc (CCL)

Economic Data: Fed Chair Powell Testimony

Wednesday, June 25:

Earnings: Micron Technology, Inc. (MU), Paychex, Inc. (PAYX),

Economic Data: Fed Chair Powell Testimony

Thursday, June 26:

Earnings: NIKE, Inc. (NKE), Walgreens Boots Alliance, Inc. (WBA)

Economic Data: Durable Goods Orders MoM, GDP Growth Rate QoQ Final

Friday, June 27:

Earnings: Shandong Hi-Speed Holdings Group Limited (412)

Economic Data: Core PCE Price Index MoM, Personal Income MoM, Personal Spending MoM

⚡ AI-optimized, human-verified: Our expert team carefully selected Premium market intelligence from Finchat.io data. Explore now →

Index Insights: How Major Benchmarks Performed Last Week

Price>MA10: 🔴

Price>MA20: 🟢

MA10>MA20: 🟢

Market Trend*:🔴

Trend Signal: 🟢

*When Price and Moving Averages are all green, the Market Trend will also be green

Price>MA10: 🔴

Price>MA20: 🟢

MA10>MA20: 🟢

Market Trend: 🔴

Trend Signal: 🟡

Price>MA10: 🔴

Price>MA20: 🟢

MA10>MA20: 🟢

Market Trend: 🔴

Trend Signal: 🟡

Sector Performance: Winners and Losers from Last Week

Put the market on autopilot, experience the Best Platform with TC2000

Explore now →

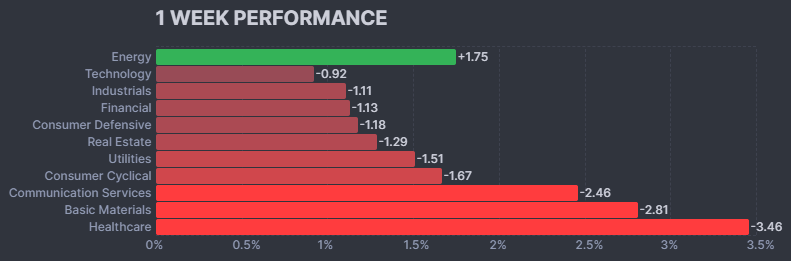

Winners

🛢️ Energy (+1.75%)

Energy led the market this week with a 1.75% gain. This growth reflects strong investor confidence, likely driven by stable commodity prices and a positive outlook on global energy demand.

Losers

💻 Technology (−0.92%)

Technology experienced a slight decline of 0.92%, possibly due to profit-taking or a shift in focus toward other sectors.

🏭 Industrials (−1.11%)

Industrials fell by 1.11%, reflecting concerns about potential economic slowdowns and their impact on manufacturing and infrastructure.

💰 Financial (−1.13%)

The Financial sector dropped 1.13%, likely due to uncertainties surrounding interest rates and tightening credit conditions.

🛡️ Consumer Defensive (−1.18%)

Consumer Defensive stocks declined by 1.18%, suggesting a rotation away from safety stocks as investors explore riskier opportunities.

🏢 Real Estate (−1.29%)

Real Estate slipped by 1.29%, possibly due to concerns about interest rate sensitivity and evolving property market trends.

⚡ Utilities (−1.51%)

Utilities saw a 1.51% decrease, indicating reduced demand for this traditionally defensive sector amidst market volatility.

🛍️ Consumer Cyclical (−1.67%)

Consumer Cyclical stocks dropped 1.67%, signaling reduced consumer spending on non-essential goods.

📱 Communication Services (−2.46%)

Communication Services faced a significant decline of 2.46%, likely due to competitive pressures and shifting consumer preferences.

🧱 Basic Materials (−2.81%)

Basic Materials fell by 2.81%, reflecting concerns about industrial demand and global economic activity.

🏥 Healthcare (−3.46%)

Healthcare recorded the largest loss of the week, dropping 3.46%. This decline may indicate reduced investor interest in defensive sectors amidst broader market shifts.

🌟 Weekly Industry Leaders 🌟

📈 Grocery Stores (+7.30%)

Grocery Stores led all industries this week with an impressive 7.30% gain. This surge reflects strong consumer demand and resilience in the retail food sector, positioning it as the top-performing industry.

🌾 Farm Products (+5.09%)

Farm Products posted a solid 5.09% increase, driven by robust agricultural demand and favorable market conditions. This performance underscores the sector's importance in the global supply chain.

💰 Capital Markets (+4.29%)

Capital Markets advanced by 4.29%, highlighting investor confidence in financial services and the broader economic outlook. The sector's growth reflects strong trading activity and asset management performance.

⚛️ Uranium (+4.01%)

Uranium gained 4.01%, continuing to attract interest as a key component of the clean energy transition. The sector's rise reflects growing support for nuclear power as a reliable and sustainable energy source.

🔌 Utilities – Independent Power Producers (+3.90%)

Independent Power Producers climbed 3.90%, benefiting from stable energy demand and the ongoing shift toward renewable energy sources.

🔥 Oil & Gas Refining & Marketing (+3.31%)

Refining & Marketing companies rose by 3.31%, supported by strong refining margins and consistent consumer demand for energy products.

⛽ Oil & Gas Integrated (+2.89%)

Integrated Oil & Gas firms posted a 2.89% increase, showcasing the advantages of a diversified business model in a favorable energy market.

🛢️ Oil & Gas E&P (+2.61%)

Exploration & Production companies gained 2.61%, reflecting steady investor confidence in exploration activities and rising energy demand.

🌱 Agricultural Inputs (+2.11%)

Agricultural Inputs advanced by 2.11%, driven by strong demand for fertilizers and other farming essentials, highlighting the sector's critical role in food production.

📊 Financial Data & Stock Exchanges (+1.59%)

Rounding out the top ten, Financial Data & Stock Exchanges gained 1.59%. This performance reflects the sector's stability and its role in supporting global financial markets.

🚀 Top Market Gainers: Crypto Deals, Stock Splits, and Strategic Moves Drive Market Excitement

SRM SRM Entertainment Inc (+706.90%)

🎮 SRM Entertainment shares skyrocketed after the company announced a groundbreaking deal with Justin Sun's crypto platform, Tron. Under the agreement, SRM will be renamed Tron Inc., and Sun will join as an adviser. The move, which includes Tron purchasing tokens, has fueled massive investor interest, sending the stock soaring.

SST System1 Inc (+141.60%)

📈 System1 Inc saw its stock surge as the company announced that its Class A Common Stock would begin trading on a split-adjusted basis starting June 12, 2025. The news of the stock split attracted significant speculative buying, driving the sharp rally.

RGC Regencell Bioscience Holdings Ltd (+125.03%)

🌿 Regencell Bioscience Holdings, a Hong Kong-based firm specializing in traditional Chinese medicine for ADHD and Autism Spectrum Disorder, experienced a massive rally. The stock more than quadrupled following the implementation of a 38-to-1 stock split, which took effect on June 9, 2025.

PXLW Pixelworks Inc (+101.88%)

📊 Pixelworks shares jumped over 100%, despite no company-specific news. The rally was attributed to a 1-for-12 stock split on June 9, which likely attracted speculative traders.

RELI Reliance Global Group Inc (+92.50%)

💼 Reliance Global Group announced a strategic move to sell Fortman Insurance for $5 million in cash. The transaction, disclosed on June 17, 2025, is expected to unlock capital for the highly accretive Spetner Acquisition. The news sent the stock climbing as investors cheered the company’s strategic execution.

🔻 Biggest Decliners: Offerings, Delistings, and Tragic Setbacks Weigh on Stocks

ICU SeaStar Medical Holding Corp (-69.50%)

💊 SeaStar Medical shares plunged after the company announced the pricing of a public offering of up to$8 million. The dilution from the offering triggered a massive sell-off, leaving the stock down nearly 70%.

GPUS Hyperscale Data Inc (-67.04%)

📉 Hyperscale Data tumbled after Milton "Todd" Ault III announced his intention to step down as an officer following the divestiture of Ault Capital Group. The uncertainty surrounding leadership changes and future direction weighed heavily on the stock.

PLAG Planet Green Holdings Corp (-66.38%)

🌍 Planet Green Holdings faced a sharp decline after unusual trading activity in its stock was flagged by the NYSE. The company issued a statement confirming no material developments or reasons for the unusual market action, leaving investors spooked and the stock down significantly.

FMTO FemtoTechnologies Inc (-59.65%)

📉 FemtoTechnologies announced that its common shares would be delisted from Nasdaq as of June 23, 2025. The delisting news caused a steep sell-off, with the stock losing nearly 60% of its value.

SRPT Sarepta Therapeutics Inc (-44.58%)

💔 Sarepta Therapeutics suffered a devastating blow after a second patient death was linked to its Duchenne muscular dystrophy treatment, ELEVIDYS. The patient passed away due to acute liver failure, prompting the company to suspend shipments for non-ambulatory patients and withdraw its revenue guidance. A wave of analyst downgrades followed, leading to a 44% drop in the stock.

🌱 Support Our Work: Buy Us a Coffee or Shop Our Services! 🌱

Your small gesture fuels our big dreams. Click below to make a difference today.

[☕ Buy Us a Coffee]

[🛒 Visit Our Shop]